Datadog IPO’d at $330m ARR, and when we last caught up with them they were already at $700m ARR — and it has done nothing but accelerate since then. Closing out with a $270m Q3’21 (!) and on to a $1.2B+ run-rate today, Datadog is accelerating at over $1B ARR. To 75% growth. Goodness.

We just haven’t seen the type of acceleration at scale we’re seeing in SaaS leaders before.

5 Interesting Learnings:

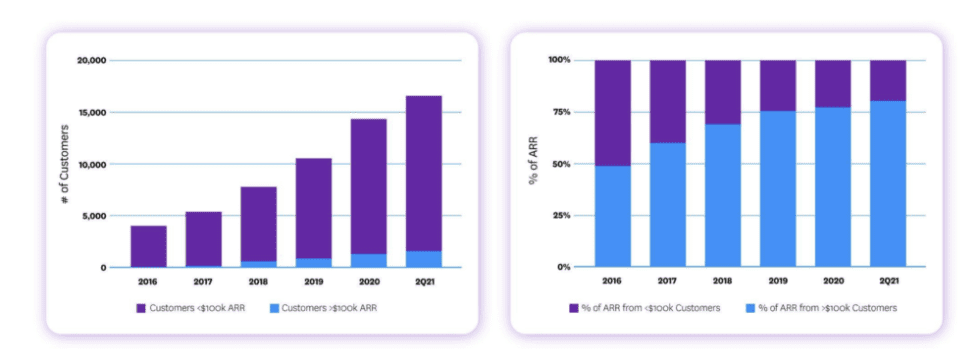

#1. 1,800 customers with ARR of $100,000 or more, a year-over-year increase of 66% from 1,082. $100k+ customers are key to ARR growth. Datadog isn’t leaving the smaller customers behind, but they are increasingly a smaller percentage of revenue. $100k+ customers have gone from 50% of revenue in 2016 to almost 80% today:

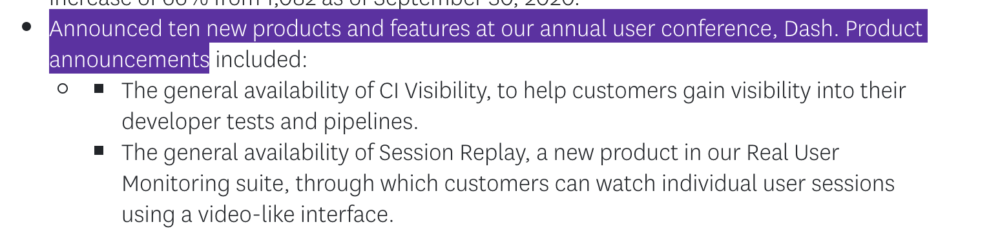

#2. More product, more products, more products. 10 new products this year. Almost all the Cloud leaders accelerating after $100m ARR, let alone $1B ARR, are multi-product.

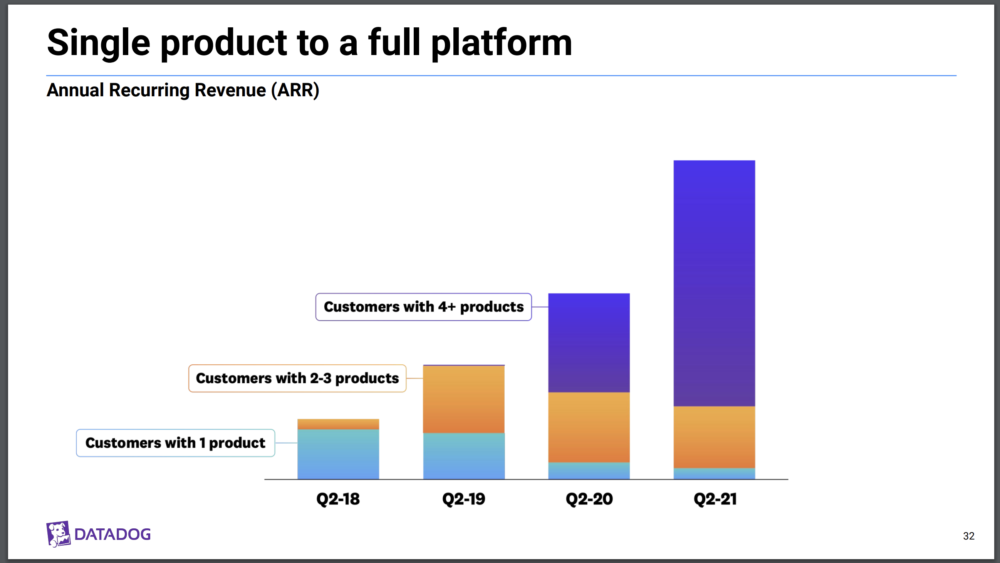

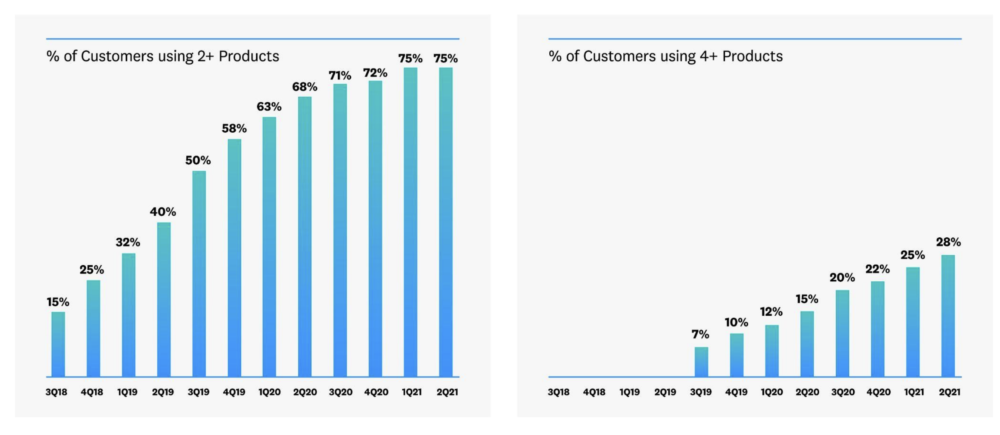

#3. In 2018, most Datadog customers used 1 product. Today, most Datadog revenue comes from customers that use 4+ products. This is one of the top keys to Datadog’s almost unprecedented growth. 28% of Datadog’s customers use 4+ products, but they make up the vast majority of revenue:

And 75% use 2 or more products, up from just 15% in 2018:

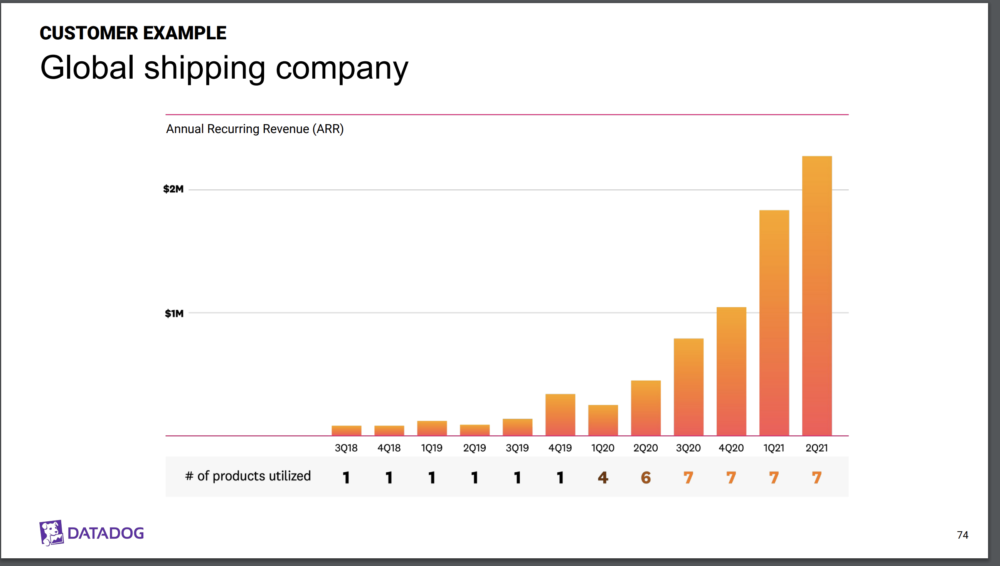

#4. Customers don’t buy all the products at first. Datadog earns customer trust, then expands products customers buy from them:

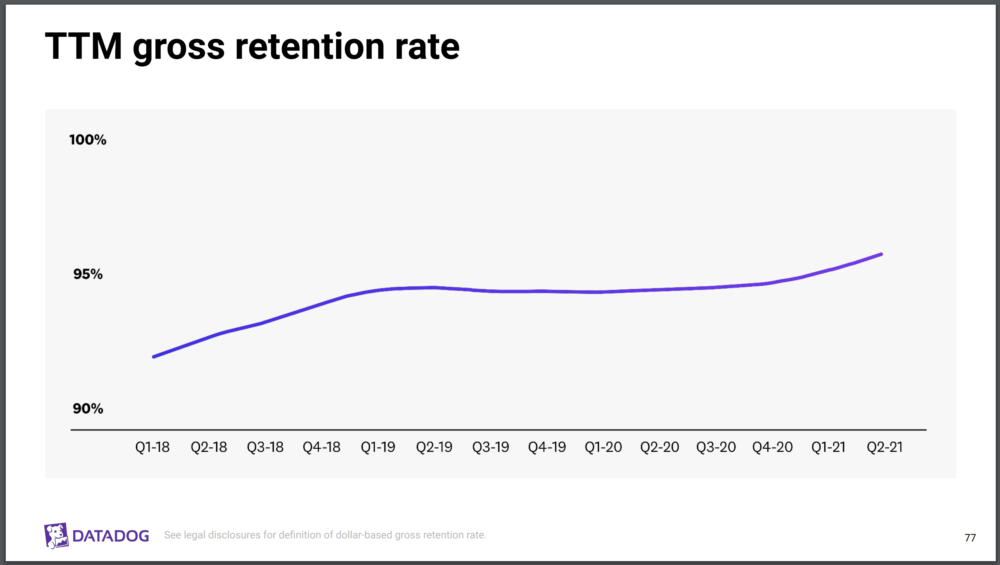

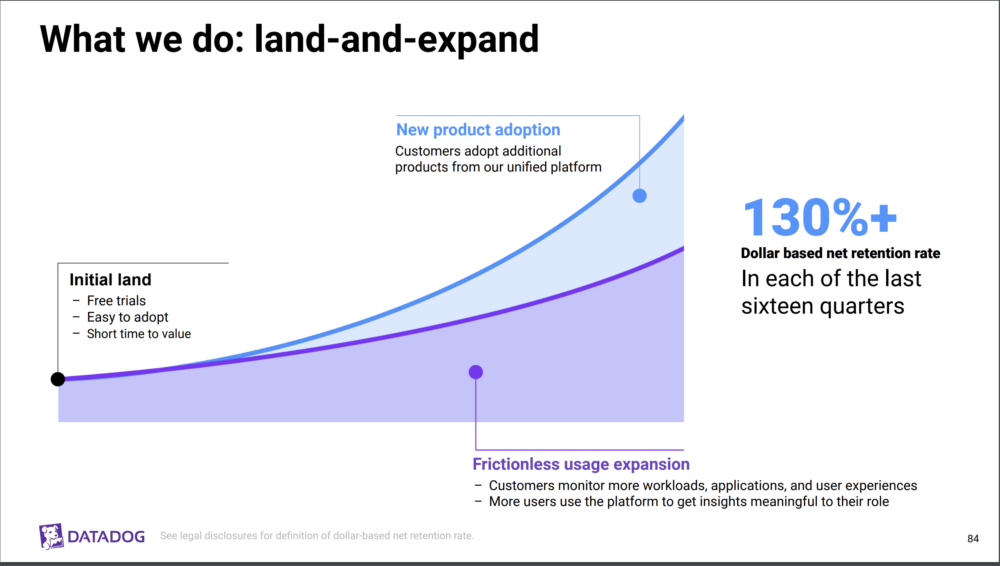

#5. 130%+ NRR for 16 quarters — and GRR going up to 95%. A reminder there is no ceiling to top tier NRR in SaaS and Cloud.

And a few bonus notes:

#6. 450+ integrations. You know this, but doing “all the integrations” can be a killer winning strategy.

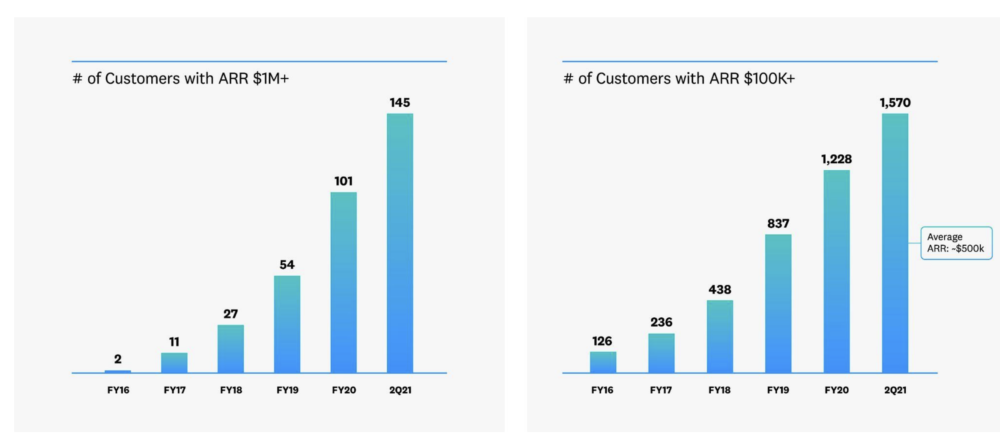

#7. From 2 $1m ARR customers in 2016 to 145 today. Datadog has steadily marched upmarket, but not abruptly.

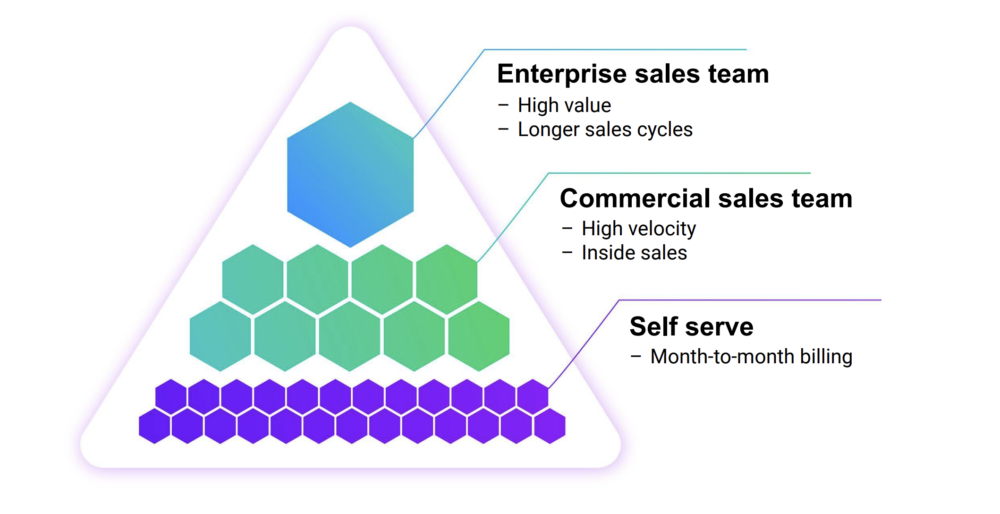

#8. A classic self-service + inside sales + enterprise sales model. Datadog may have revolutionized observability and other categories, but it didn’t change how you set up a sales team. Its smallest customers self-serve. The ones up to $50k-$100k go through inside sales. And a dedicated enterprise team handles the largest ones. Just like almost all the rest of SaaS companies pretty much with similar price points and offerings. 😉

And a great look back at Datadog just before its IPO: