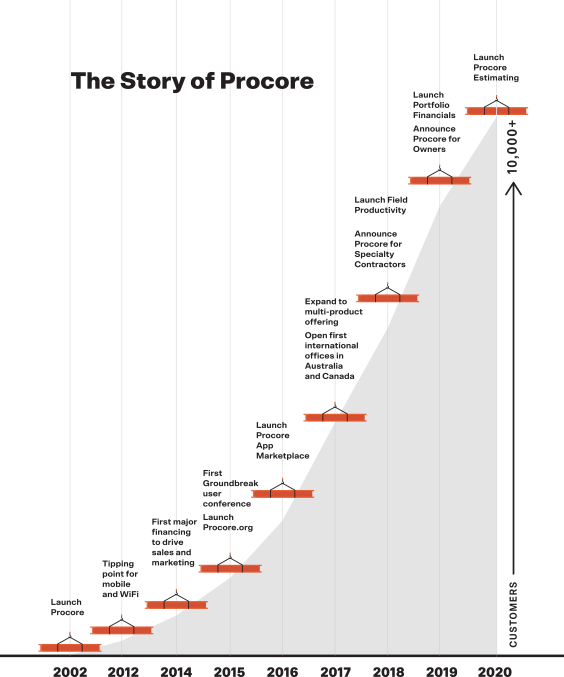

You may not have heard of Procore if you aren’t in construction, but it’s a quiet SaaS leader we can all learn from if we think about it as a break-out Vertical SaaS leader. The first 10 years were actually pretty challenging … the company was founded way back in 2002. But they hit their stride in 2012 as mobile took off, enabling construction project management software to finally really work in the field. Not just in the office.

They filed to IPO just before Covid hit and their business was impacted, as you might imagine. But they quickly bounced back and are now ready to IPO again at $500,000,000 in ARR.

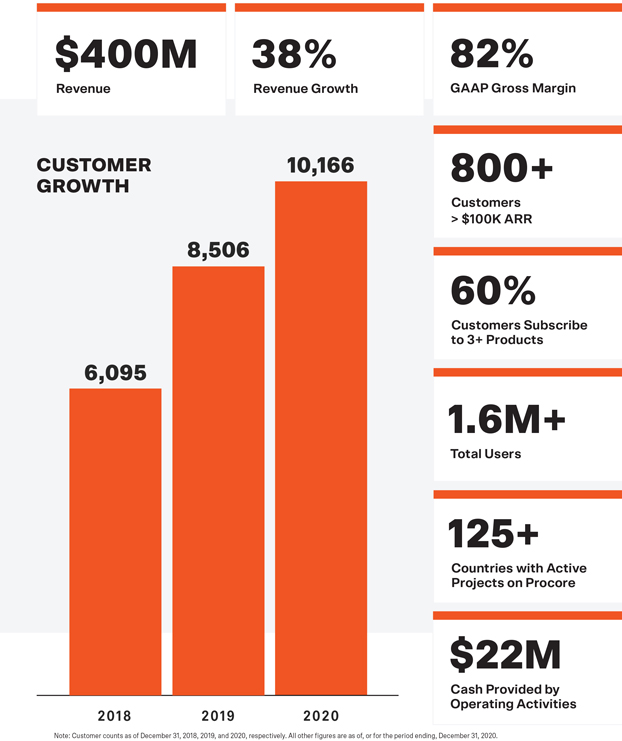

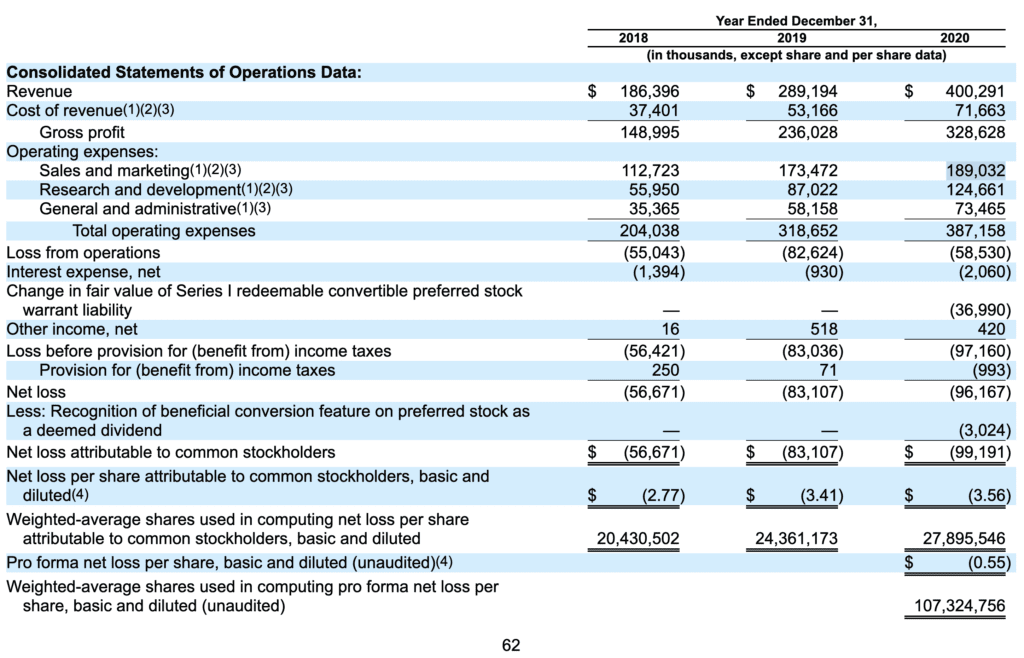

(note: precise ARR unclear, but at $400m in GAAP revenue in 2020, growing 38% year-over-year, they should be about there now).

5 Interesting Learnings:

#1. Pricing is based on products and volume, not seats. A lot of us with products that don’t naturally lend themselves to a per-seat model wonder what exactly to do. Procore has done very well aligning pricing naturally with usage. Customers pay based on construction volume on the platform (much like many APIs and fintech services) combined with the number of products customers use (intuitive to understand). 60% of its users are collaborators, and if Procore charged them, it’s difficult to imagine the adoption they’ve seen. Plain vanilla per-seat pricing is becoming less and less the dominant model in public SaaS and Cloud companies.

#2. $43k ACV across 10,000+ Customers. 92% of customers pay less than $100k ACV. Procore has embraced both mid-market and larger customers. A large deal for them is $100k+, and the big customers are 8% of their base. So while Procore serves larger customers, it has found a sweet spot in mid-market type pricing and deals at $43k ACV. The mid-market is a very powerful segment if you get good at it. Many ignore it.

#3. Customer tickets and phone calls are answered in 60 seconds or less. I love to see this called out as a strategic asset and weapon. If you do this, you win. The competition generally doesn’t. They also do not charge for support and have 5,800 tutorials on their website.

#4. Spend almost 50% of revenue on sales and marketing. While others do in SaaS spend this much at scale as well, it’s a reminder that it can also be expensive to penetrate the mid-market in a high-touch industry. Put differently, in 2020 Procore spent $190m to acquire $110m in incremental ARR (including upsells). That probably means it takes them 2-3 years for them to go profitable on a new customer.

#5. Multiple products are key to growth. We’ve talked a lot about this in our 5 Interesting Learnings series. 60% of Procore’s customers now buy 3 or more products.

And a few bonus notes:

#6. 250 Partners on its App ecosystem. They view this as one of their most important platform features. Vertical SaaS needs an ecosystem, too. 81% of their customers use at least 1 integration, and 60% use 2 or more.

#7. Founded in 2002 by Tooey Courtemanche, who is still CEO. Tooey started the company in 2002 and served as its President for the first few years, and again since in 2019. Go long, folks. He owns 6% at IPO. (Iconiq bought up an impressive 40%.)

#8. Slow to go international, but now a force. Procore didn’t really expand outside of the U.S. until 2017, but then it did so aggressively. Now, 12.2% of their revenue is outside the U.S.

#9. New customer growth isn’t fully back to pre-Covid levels. New customer count is still impressive and has substantially recovered from the post-Covid drop. But they are still impacted (as one might expect). Still, growth from the existing base has made up for it in many ways, allowing a return to an incredible 38% growth at $500m in ARR.

#10. NRR took a big Covid hit — But it never fell below 100%. Procore’s customer base was hit hard by Covid, and NRR fell from 117% to 107%. Still, it never fell below 100% … even at the lowest point after Covid. Now that’s the power of recurring revenue!! And gross retention stayed high at 95% — the same as pre-Covid. So even if customers spent less when things got tough, they didn’t stop spending with Procore. They stayed even in the tougher times. GRR is as important as NRR. A bit more on that here.

Wow, what a story!

In 2002, we founded @procoretech w/ a mission to connect everyone in construction on a global platform. Today we celebrate Procore’s IPO and the exciting future ahead. I am humbled and honored to serve the construction industry that builds the world around us. @NYSE #ProcoreIPO pic.twitter.com/MQgUGPpnKh

— Tooey Courtemanche (@tooeyprocore) May 20, 2021