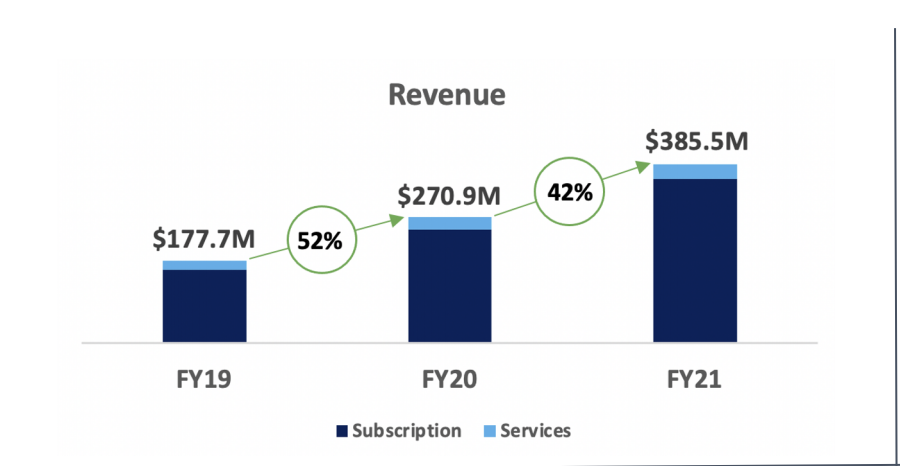

We’ve done a lot of fun sessions together with Smartsheet over the years at SaaStr but haven’t taken a deep dive into its business. It’s an interesting one, with a very broad base of SMBs and a slow-and-steady path to going upmarket. They are now growing a stunning 42% year-over-year at over $400,000,000 in ARR!!

Founded way back in 2006, adoption was slow at first, but they kept at it and Smartsheet is now growing faster than ever 15+ years later.

Let’s take a look at 5 Interesting Things:

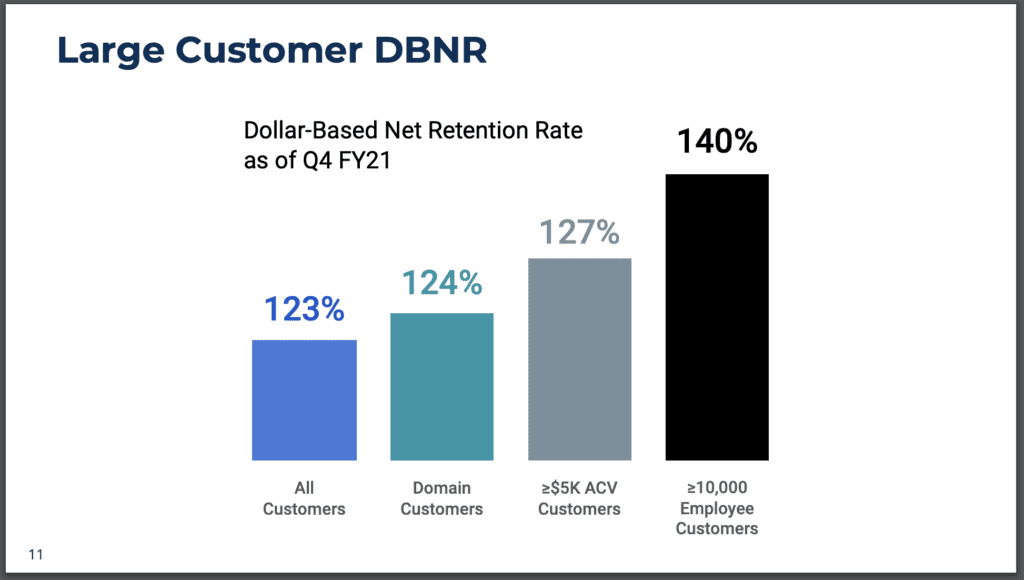

#1. Very High NRR from SMBs. Smartsheet has a very impressive 123% NRR from SMBs. They also nicely segment NRR by deal size, so you can see it grows to 140% from their largest enterprise customers.

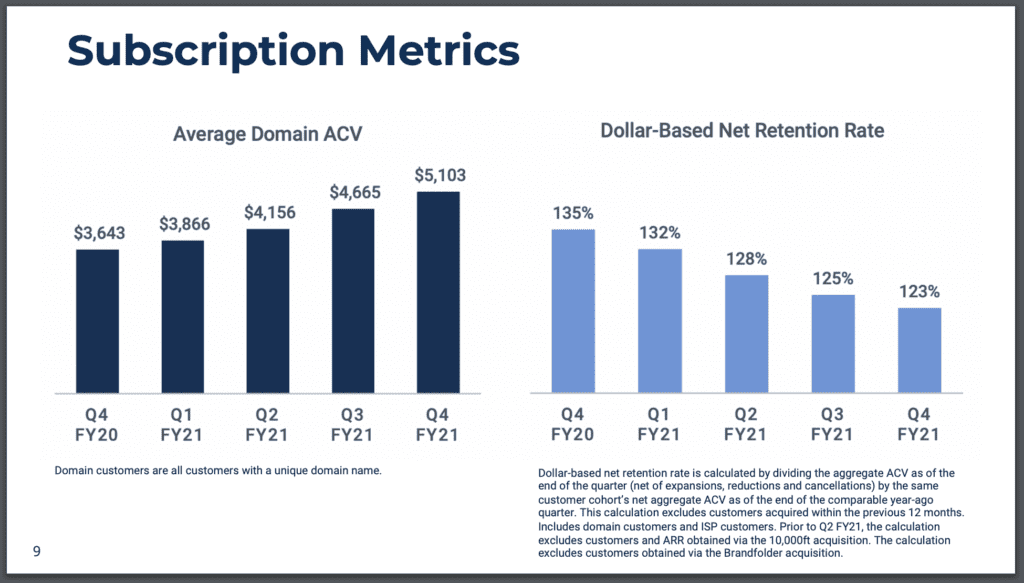

NRR has come down a bit over time, from 135% pre-Covid to 123% today (as you can see below), but in any event, is world-class for SMBs.

#2. Driving deal size up accounts for a lot of growth. Smartsheet has aggressively driven its ACV up from $3,643 in 2020 to $5,103 today. That’s a lot — 40% higher average deals. This just about equals their ARR growth.

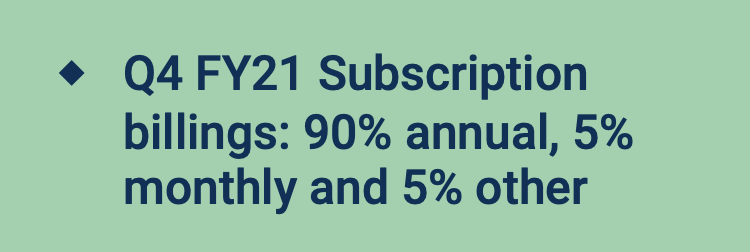

#3. 90% of customers pay annually — even SMBs. This is an interesting contrast to Zoom, which has seen its monthly invoicing grow to 50% of its $4B+ in ARR. It just shows perhaps there is no standard answer to how often SMBs should pay.

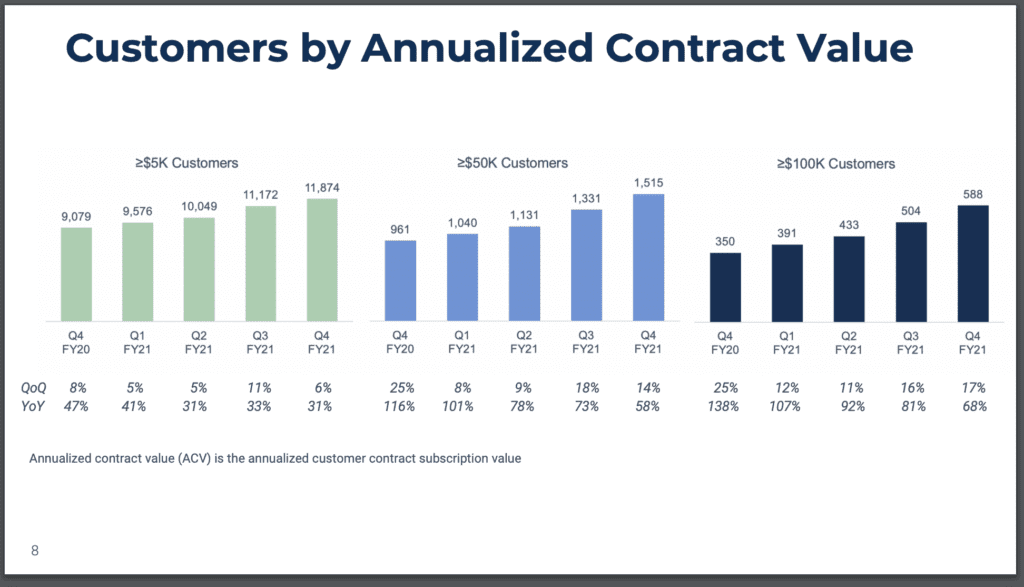

#4. The biggest customers are fueling the most growth. Smartsheet, like PagerDuty, Asana, and a few others in this series waited a while to go “more enterprise”, but then leaned in. At IPO, Smartsheet was all about SMBs. Today, its fastest-growing customers are $100k+ deals:

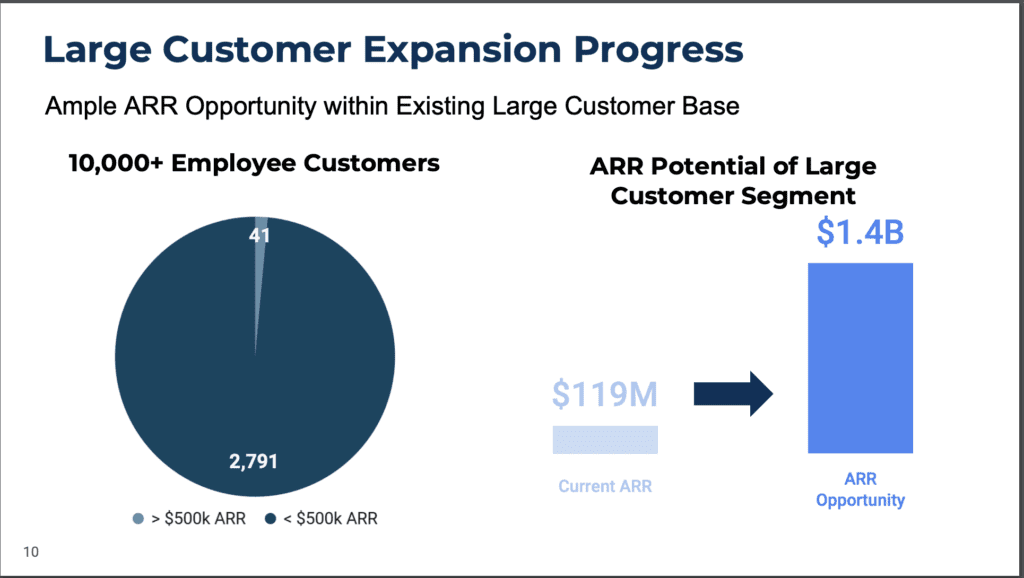

#5. A big bet on $500k+ deals. Smartsheet’s next push is $500k+ deals at 10,000+ employee customers. The overall productivity space has plenty of room here, but it’s a different pace and feature set and it will be interesting to watch Smartsheet’s progress on the way to $1B in ARR.

What a great story! A patient run over a decade to $100m ARR and then IPO, and then a push into bigger deals at $150m+ ARR, and then deeper into the enterprise at $400m-$500m ARR and beyond.