A while back, we wrote a post on SaaStr that made a lot of folks a little angry: “Workday is growing 90% this Year. At $250m in ARR. So Wake Up. You Probably Need to Do a Lot, Lot Better”. Looking, back it was a rather aggressive headline 🙂 And more importantly, people were upset because Workday was seen as a complete outlier. You take the founders of Peoplesoft (acquired for $10b), add infinite capital, and do a re-do in the same space … well of course you’ll have an outlier, people said. Not fair. We can’t possibly do as well. Not a fair yardstick.

OK. Let’s fast forward to today, and figure out what is “fair”. Let’s look at the latest SaaS IPOs and IPOs-to-be.

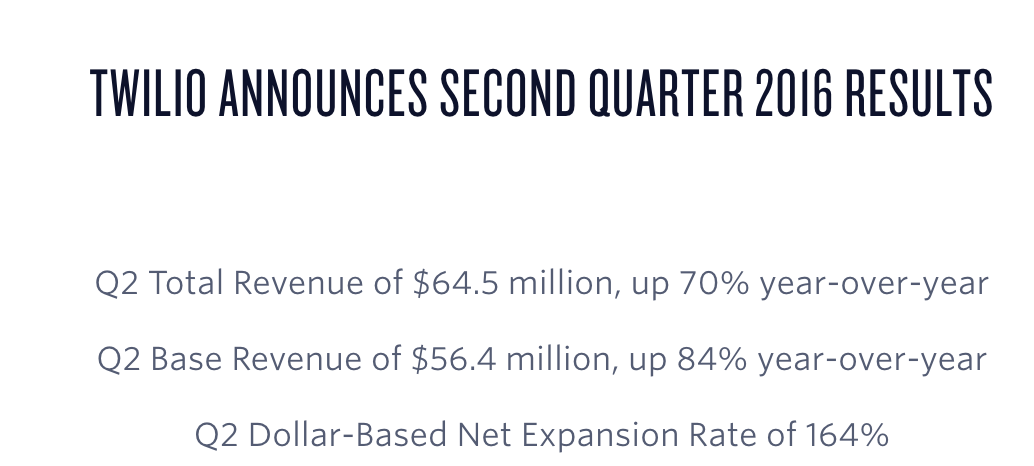

Let’s start with Twilio — the most successful tech IPO of the year. Twilio went public when the consensus view was the IPO window was barely open. So Twilio priced low (which was smart), exceeded expectations in the next quarter, and thus, has appreciated 250% since the IPO. Boom!

But to me that isn’t interesting. That’s just a price for a share of stock. What’s interesting to me is using Twilio to help us think about: What’s the Bar for SaaS Success going into 2017?

So let’s de-pack Twilio’s growth at ~$300m ARR:

Growing 70% year over year, folks.

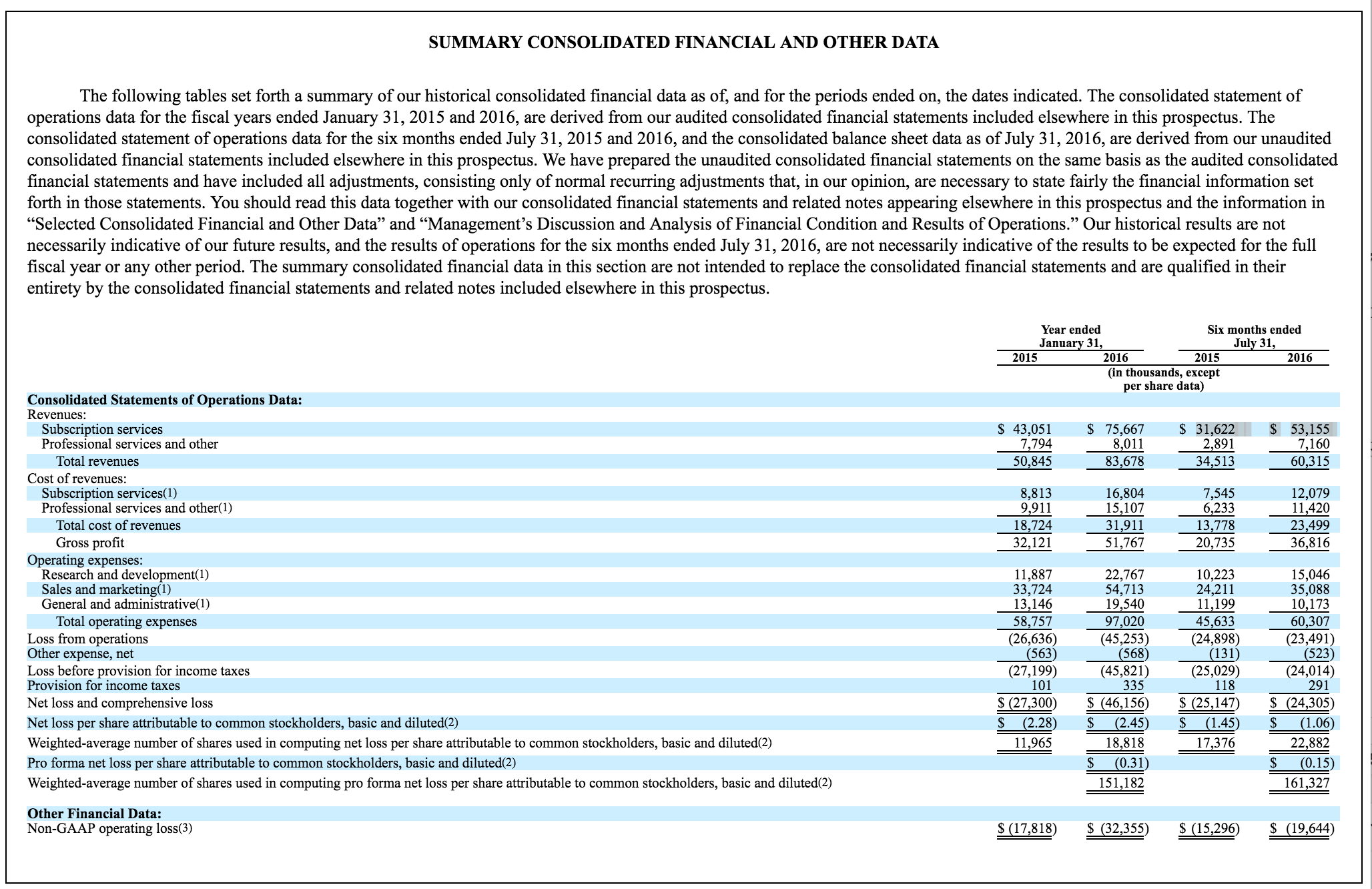

Now let’s fast forward to the latest private unicorn SaaS company to file to go public, Coupa. Coupa just filed, but we do have the financials through Q2’16:

And what do we see again? Growing 70% year over year, folks. Here, probably at $140m ARR or so, vs. $200m+ when Twilio filed. But still, well past $100m ARR and still growing 70% YoY.

The two companies are no doubt, different. Twilio has been more capital efficient. Twilio has a radically different go-to-market, as an API service, and a jealousy-inspiring amount of “automatic” expansion in accounts (you use more, you pay more). Coupa by contrast is a classic enterprise business process management solution, for procurement and spend management, founded by seasoned Oracle veterans. It also took a lot longer to get there than Twilio.

And the two companies are also probably different than your company. They are both in established, very large spaces. Yes, Twilio did something very disruptive and new in providing a super developer-friendly voice API and service. That was new and cool. But at a meta-level, telephony itself, voice, is one of the largest categories of “allocated spend” in corporations. And importantly — something customers are trained to pay for and value. (I’ve watched this also fuel hyper-growth at Talkdesk). Similarly, Coupa’s space — procurement and spend management — is a classic, large category of enterprise software (see SAP, Ariba, etc.). Large companies are willing, and perhaps even more importantly, forced to, spend large amount of money to manage the billions in products and services they buy. And have been doing so for decades. Put differently. Both Twilio and Coupa have access to a lot of existing buyer budget.

But here’s my take-away. It’s the same take away from when Workday IPO’d, and I admit, it’s a little annoying to hear. But. The markets are bigger than ever in SaaS, folks. Much bigger. Like 500x bigger than 10 years ago. Like 10x bigger than 5 years ago. So … You can do better. Especially if you have happy customers and product-market fit. That’s the hardest part today. Too many vendors, too many products. If you’ve gotten past that, have true (even if early) product-market fit and have high NPS … you are golden these days. Even if it doesn’t feel like it.

If Twilio and Coupa can grow 70% Year over Year as they breeze past $150m in ARR … why should you settle for 60% growth at $8m in ARR? Or 100% at $4m in ARR? You shouldn’t. Don’t settle.

Your market is being disrupted just as much as telephony and spend management are. Sales, marketing, software development, CRM, ERP, enterprise video, search, QA, fleet management, e-discovery, recruiting, performance management, you name it. It’s all going through a SaaS/cloud disruption. That disruption means there absolutely, positively, are another 50-100 customers out there for every single one you have today. There is no chance you have maxed out your market. There isn’t.

And if the law of so-called large numbers didn’t stop Coupa and Twilio at $150m ARR, it certainly shouldn’t stop you at $15m ARR, let alone $5m.

So there is no excuse for not growing faster.

Here’s my real point. Whatever your growth rate is today, don’t accept it. Don’t accept a Q4 than isn’t at least 50% bigger than Q1. Don’t accept growth rate < 100% — ever. Not until you are huge. This doesn’t mean you have to beat up your team. Maybe it’s too late to impact this year, and maybe changing the plan too aggressively for next year is too daunting for the team, today. Maybe. Maybe this is only a conversation you have with your co-founder, in quiet, privately.

But the markets are bigger, faster, and stronger than ever in SaaS. It just takes a small migration of the $1 trillion in IT spend to create scores of IPOs. Just tapping into a tiny bit more of a larger-ish market will easily get you an extra $1m, $3m, $10m in ARR.

I mean, look, 10,000 founders, VPs and VCs came to the SaaStr Annual ’17. Ten thousand. How is that even possible? I never would have thought. It’s because everything is bigger in SaaS these days, folks.

Go forth and conquer! You can do it. And don’t settle for 2011-2015 growth rates, anymore.